Keeping the Lights On: A Guide for Saas Finance Teams to tackle CoVid

Click to Read

Introduction

COVID-19 is a tumultuous time for businesses. The time is wild and chaotic, and your finance leaders are sitting on the hotseat clouded with uncertainty.

This comprehensive guide is an interview compilation of the webinar series - Keeping the lights on. It is curated for finance leaders to reconstruct their strategies for 2020 and forward. It is segmented into five sections, each section focussing on a specific topic: budgeting, forecasting, cash-burn, payment and contracts, and data analysis.

You can read on for key takeaways or watch the interviews here.

Surviving the crisis by cutting spending without lay-offs

We're in the middle of a global pandemic, a health crisis that's turning into an economic crisis. The situation is critical, and companies are taking actions across the board. The real problem though is that we don't know how long this will last. If it lasts for a month or two then the actions taken by companies might seem drastic - if it drags on, then they might seem timely.

Finance leaders should learn how to budget effectively to budget effectively instead of feeling stuck. With the patterns changing, they need to quickly adapt their budgeting patterns for today's need.

Anders Liu Lindberg, COO and CMO at Business Partnering Institute, throws light on how to budget effectively during this crisis, what to keep in mind when you're budgeting and innovative ways companies can cut spending.

How to budget effectively?

We cannot dispute the fact that even well-run companies are going bankrupt. Suppliers in the hospitality industry, they had to shut down their entire business overnight. At best they planned to cut out 70-80% of their staff and if they trudged along the bad waters for too long, they simply had to close their business. You can imagine the hot seat their finance director was sitting on.

But after speaking with a SaaS company selling consolidation software, I got to know they were doing okay despite the crisis taking its toll. Their customers kept paying in spite of sales being down. To top it they were announcing new customers in the middle of the crisis. The realization dawned on me: Businesses with a recurring model were able to perform better than their counterparts who're dependent on the physical element.

Many companies are feeling the crisis in different paces from day one spilling over into every passing day. It's only natural to feel like the Lehman Brothers in this crisis! This means your plan A, B, and C made at the beginning of the year feels useless and now you're in a prolonged survival mode. Here are a few tips on how you can restructure and budget effectively.

All spending is in scope to be cut and fast

The crisis has gotten companies going into cost-cutting modes to curb spending. Businesses working closely with the most affected sectors (example given above) are facing the wrath of this pandemic. Even though many businesses are laying off their workforce, this might not be the most effective option. In many countries, you've got a notice period of 1-3 months. So how does that help in the shorter-term? The truth is that it doesn't. It will only help if the crisis lasts longer or you were planning to do these cuts anyway.

All activities that are not business-critical are naturally in scope. That means most project work and investments (especially if they're not committed) will be shut down or at best postponed for later.

All non-salary SG&A costs will be in scope and while traveling is a distant possibility, temporary workers and consultants will have their contracts terminated early. Employee benefits are also in scope, so the Summer party is gone, there is no more teambuilding or bonuses waiting to fill your bank accounts (as the business results take care of that).

Companies aren't spending unless they're legally obliged to or if it is business-critical. Every other cost that's not immediate is put in hibernation as companies try to survive the crisis and hopefully emerge in better shape than their competition.

Is laying off people the right course of action though?

It's too early to say if lay-offs are the right option to save the businesses. But if we're looking at a V-shaped recovery then laying off people will put you in a very poor situation. This is because once things regain momentum, it'll be difficult to re-hire fast. You'll be scaling slowly in comparison to your competitors impacting your future growth.

A better way forward is to temporarily cut salaries like how many companies doing. Alternatively making use of government-sponsored plans to send people home with pay. In this case you can simply pick up work again once the crisis is over. If the crisis doesn't pass soon the risk is about how little you've done and it might be late to lay-off people.

Considering twice before laying-off your employees is the right way to go! Re-hiring will be troublesome in the future as your brand will be taking the damage. People might be cautious before applying because they would want the companies to be sticking with them through thick and thin.

Digitalize and automate as much as you can, even your mundane administrative tasks! Processes like accounts payable and receivables are clear targets for automation. Many tools are available today. If you've not thought about it this crisis can be your catalyst to consider this to create a mid- to long-term benefit.

What's the role for finance and accounting?

This is a real question for all the finance and accounting professionals out there. How are you going to lead your company through this? When times are bad, management teams typically look to the CFO to save them and so shall the CFO.

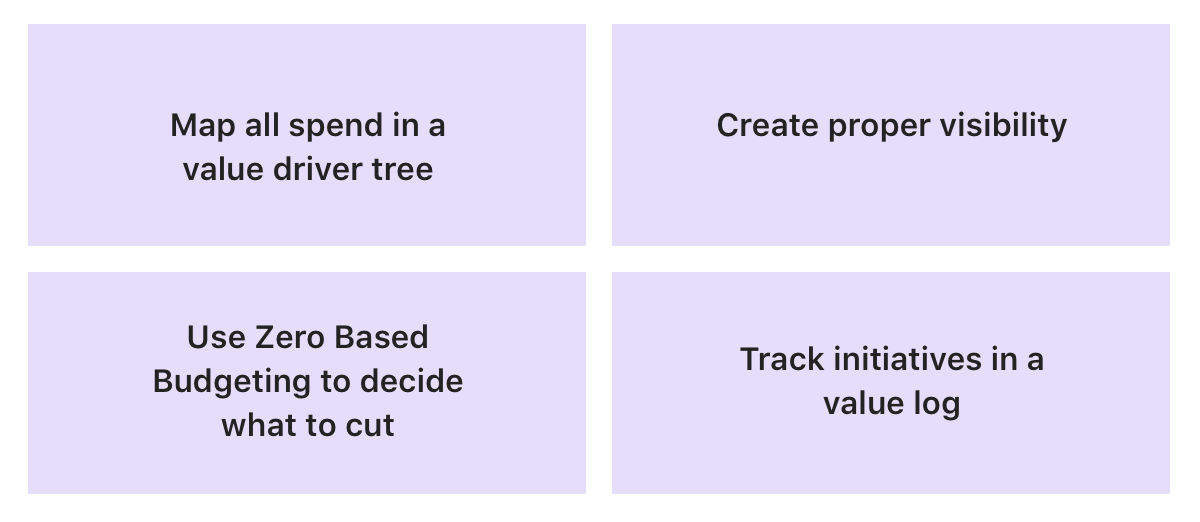

However, it won't happen without the use of good tools. Firstly, you must be sure to map all your spending categories into a value driver tree. This value driver tree goes beyond your P&L spending and into your balance sheet and your company risk profile.

The net working capital, for instance, would be a good place to look.

How likely is it for companies to start cutting or freezing their subscriptions? What you thought was recurring revenues bound by contract are no longer there.

How likely is it for companies to offer deferred payment terms? For example, from 30 days to 60 days.

After having a clear picture of how value is created or destroyed in your company. It's time to pull out the big knife, clear the table and start from scratch. A good tool to build up a minimum viable budget is to use Zero Based Budgeting. There's no better time to truthfully answer the question "what do we really need to run our company".

It's very important when doing these exercises that you have proper visibility into how your numbers are moving. If you can't see the impact of your initiatives, you're likely to fail in your efforts to save the company.

A good dashboard with all spend categories in real-time (or at least weekly) is a good first step. Here you're not looking at accounting numbers but rather purchase orders, credit card activity, etc. anywhere which helps you find out if your spending is coming down or not.

The last thing you can do, especially for more structured initiatives, is to create a value log where you track the impact of each initiative you take. While your general spending dashboard will tell you if the overall direction is right or not the value log will tell you whether specific initiatives are successful or not. If you see one initiative failing, for instance, you might decide to act regardless if the overall numbers are good or not.

Lastly, a value log will also help you facilitate an after-action review once the crisis has passed. What worked and what didn't and what can you do differently next time crisis strikes?

Reforecasting and rebuilding revenue projections in the COVID world

Forecasting your revenue to the exact is impossible during these trying times. Financial markets are gyrating and there is no particular path that shows how markets will recover. Looking back at the 2008 crisis, some companies revised their annual projections almost 6 times. It's important to look at key assumptions that matter to make your forecasting model dynamic to changes.

Matthew Wensing, Founder of Summit and former board member at RiskPulse, answers questions around managing cash-burn, mitigating non-essential expenses and effectively forecasting revenue for the rest of 2020

What is the current state of forecasting in the COVID world

MW: Forecasting is done based on assumptions and those assumptions are the key.

The new thing about this landscape is that the baseline has moved and we don't know how much our baseline has moved. It's always best to be more aggressive up front and assuming how bad things might be in terms of the new world we're in.

The other side of this situation is that we're not sure how long we're going to be at that bottom of the trough. If it seems long enough, ask "How long will this last for?". That would be the other major assumption going into this model. And then look at which road back to the new normal are you also assuming is going to occur? Is it going to be fast? Is it going to be slow? Will it be sooner? Will it be later?

The general takeaway from this would be, anytime you're talking about a forecast you need to have clarity on the assumptions you're making about each of those.

To be clear about a forecast you need to know the answer to these three questions: how bad is the new baseline, how long will we be there? And what are we assuming about recovery?

How to think about forecasting for the current scenario?

MW: Learning how to forecast is important as traditional methods might make little relevance.

In these uncertain times, it's better to have more scenarios than have a few that are very nailed down. Having more scenarios at hand will help you be clear about what your assumptions are for those.

In your weak case, strong case and best-case scenarios, you need to have your assumptions branching into them. In addition, you need to make other decisions about how bad will it get, how long will it last and what does recovery look like?

The goal right now should be is to see a breadth of possibilities cropping up and not to zero in on one.

Forecasting across industries

Some businesses are closed and some open. Looking at this scenario in terms of forecasting is how many pricing models depend on the growth of their customers to drive upsells and growth? And to the extent, you have a model like that, which is highly dependent on the success of your own customers in terms of their revenue to pay you more.

Segmenting your customer base by industry and mapping how their revenue has taken a hit can help you in determining your revenue.

How to reassess your numbers for 2020?

MW: Numbers that made sense at the beginning of 2020 seem to be less applicable now. The forecasting should be done for the entire year and not for the immediate quarter, Here's why:

Reassess your numbers for 2020 as a whole. Even though firms like Morgan Stanley released guidance saying the economy's going to bounce back in Q3, et cetera, no one really knows what that road is going to look like.

It's good to know what the path to normalcy looks like. That's the third key assumption. It's good to keep in mind that ramps are everywhere.

And if you look at timelines, you need to think about how long it will take to find that new recruit, how long will it take to onboard somebody? How efficient are people going to be at their work or how productive are they going to be at their work?

In a poll with 200 respondents, some of them said they're more productive at home as It saves their commuting time. The rest 50% said they're as productive as before or worse. In this case, we don't know how long it'll take to bounce back and it's certainly not happening in 12 weeks.

You have to look at the entire calendar year and I think you have to really decide what's going to take longer than it used to take. And there could be some long cycles to that. The goal right now is to sustain the current situation

How to forecast based on your customers/subscriptions?

MW: Cohorts and survival curves are an extension of your funnel.

In these times treat your new customers as a potential customer who would be with you for a longer-term. With many companies cutting costs, if customers' are signing up now to your product, they look at your product as a need and not a want. It is something that matters to them.

Double down on the potential of your customers and treat them as if each one was a 5x or 2x opportunity because it's a strong signal to sign up this month or next month given the situation.

What are the indicators that help determine financial impacts on your business?

MW: Metrics are vast and drilling down on each of them leads to confusion. Replace the now defined forecast with your previous existing metrics.

Determine your metrics and skip looking at vanity metrics. Back in the day you might have rolled eyeballs for page views and thought your numbers were up. But, things are different now. If you want to take a lean approach, remove all the vanity metrics, which means any metric that you don't understand, that you don't know for sure will mean positive progress for your business.

It's always good to focus so that you don't lose key indicators over ones that are noise. In times like these, there's a lot of noise and volatility.

Reduce the number of numbers you're looking for and just look at the ones that indicate progress and retrench to the ones you're confident about.

Stop-gap plan 2020

COVID-19 is a black swan event taking businesses by surprise. Most businesses now should be protecting their employees, their business, understanding the risks and managing their cash in accordance with the disruptions caused by the spread of COVID.

In times like these, Cash is king. Companies should develop a good treasury plan for cash management by taking into account the end-to-end disruptions and preparing for the worst case.

Ben Murray is the CFO and Vice President at Cartegraph. He's a corporate finance executive with over 20 years of experience with private and public companies. Ben has been a SaaSCFO for the past eight years blogging about SaaS finance.

Ben throws light on cash-flow analysis, scenario analysis and looking at metrics that matter.

Cash flow analysis

Cash flow analysis, in simple terms, is the amount of money flowing in and out of your business. It measures the liquidity of your business. Analyzing your cash-flow is important during normal times, but during these volatile times, it should garner extra attention and focus.

BM: Cash flow is measured as net cash flow and gross cash flow. It helps to analyze if you're burning cash or building cash. Cash flow is the major reason why many businesses fail during good and bad times. Hence, it's crucial to understand cash runaway. I like to look at cash burn like no invoicing was being done, in simpler terms, no cash is coming in.

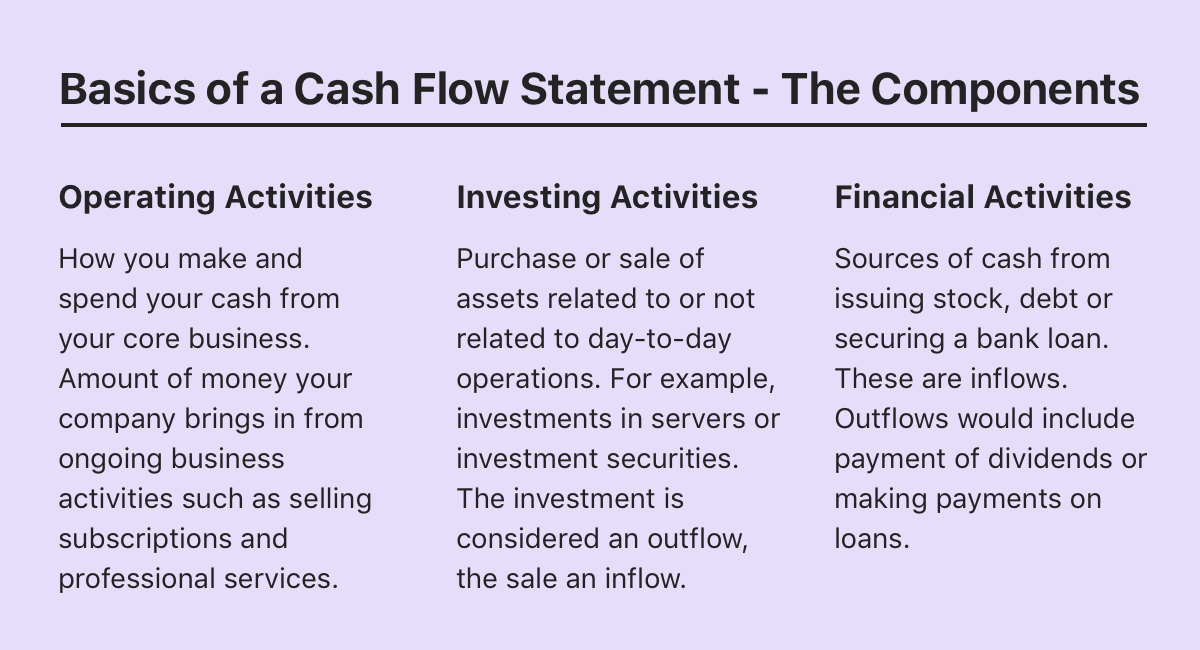

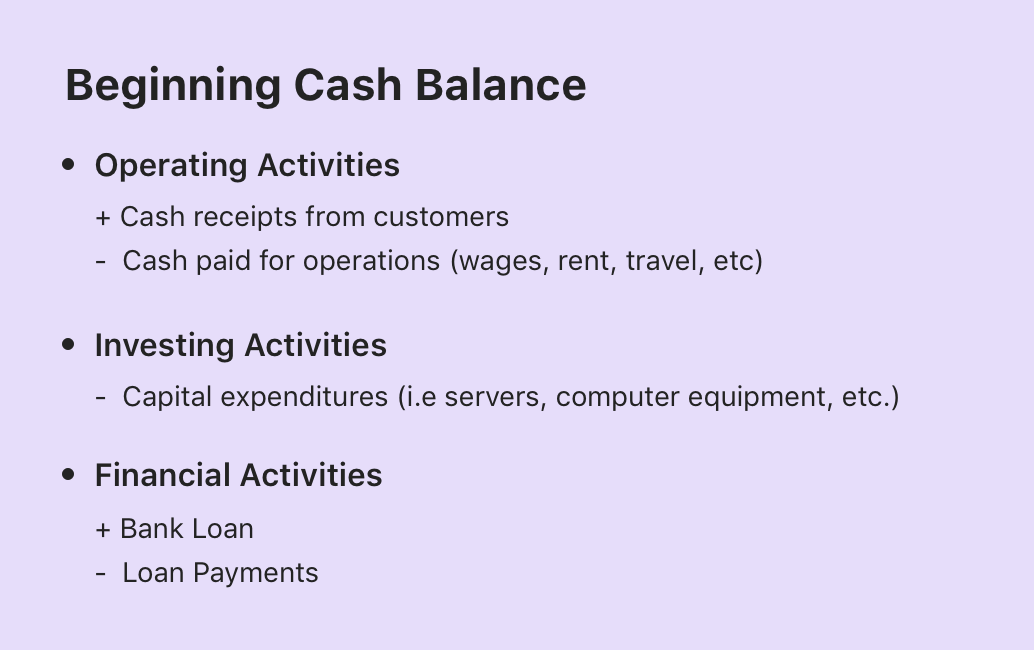

To calculate, look at your current bank balance and divide it by monthly operating expenses. This will give you an idea of how many months of cash runway do you have? If your business didn't invoice anymore, how long could you thrive with the runway amount? Delving a bit deeper into cash-flow, these are the main components you should be looking at,

These areas are our core business activities and ties down to the invoices we're sending out to customers. The first is "operating activities", which covers the operating expenses such as wages, rent, etc., Then comes "investing activities". If you're investing in servers, internal R&D, etc., From the "financial activities" perspective, it could be cash coming in from loans, stocks, or just principal payments on our term loans.

Getting started with cash-flow forecasting

BM: You don't need a full financial model to forecast your cash-flow. Think about the cash receipts from your customers. Assess their paying methods, if it's recurring on credit cards or if you're invoicing and collecting that cash.

Look at cash paid from off operations, wages, rent, travel, investing, etc., Are you doing an investment that's not hitting your P&L in a non-cash way but hitting your balance sheet? Then look at your capital expenders on servers, computer equipment, internal R&D and your financing activities. Do you have debt or loans? Are you making principal payments?

All these need to be included in your cash-flow to calculate your ending cash balance. This doesn't have to be complicated, just look at the major investment buckets within your business. Look at your working capital which throws a huge focus on accounts receivables and payables.

Scenario Analysis

Scenario analysis is the process of making business assumptions based on internal and external factors that affect the financial trajectory. Doing a scenario analysis will help you be prepared for any kind of situation you'll encounter over the next few months.

BM: During times like these, a scenario forecasting must be done with a weekly cadence. This is a great method because it'll help your business prepare for the future and be proactive, while you still have cash. In this process, you stress test your business. For instance, I run through worst-case assumptions. I keep my expense base the same and forecast by reducing booking revenue and increasing churn. This helps me analyze what these implications do to my company's margins and cash.

If cash gets tighter, then you can focus on your outbacks to determine which can be delayed or eliminated to increase your cash runaway. Also, focussing on the 80/20 rule will help you understand the major trigger that affects business. If you're a couple million in ARR, it's time to implement monthly forecasting in your business. This is a great financial discipline to have.

In times like these, we should be forecasting as our business and the external market is changing. Historically once a month would've been apt, but now, it's good to do it weekly. It also ties down to how fast your assumptions in financial planning is changing.

As a rule, I like to forecast for the worst and the most likely scenarios. This helps determine if your cash runaway shortens or lengthens. Thus, enabling you to take proactive financial actions which will extend your cash runway.

Metrics that matter

In a sea of metrics, you need to focus on the ones that matter the most, now. This being a difficult time, it's easier to get lost in metrics that don't add value to your business. By doing that, you'll be entering a landslide of inaccurate forecasting and financial management principles that'll take a toll on your business health. Ben tells us which ones should have our utmost focus during these volatile times.

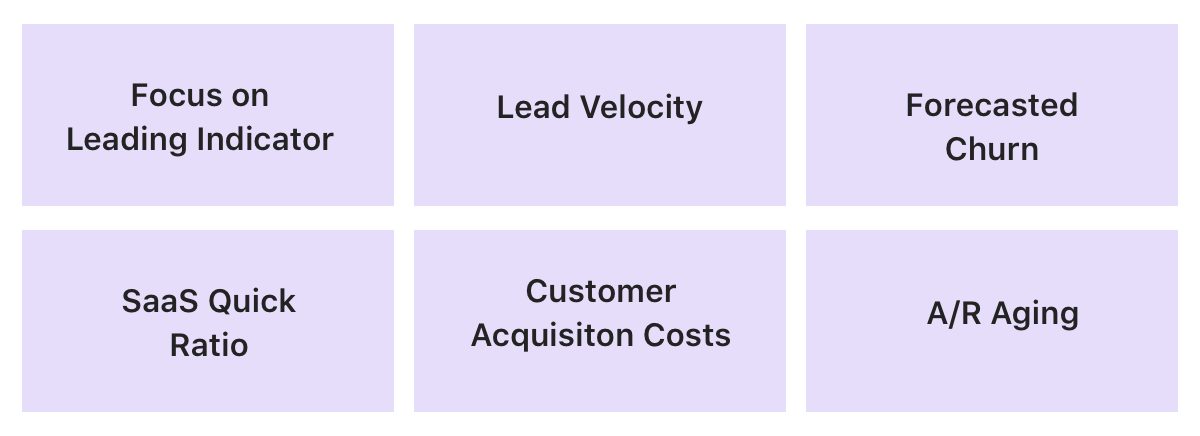

BM: Focus on indicators that give you an advance warning of what's going to happen to your business. If your GTM model is inbound traffic, you'll know as traffic declines in your trial sign-ups, etc. If you have the outbound model, then you might not be getting leads coming in, which is a leading indicator for your pipeline failure.

Lead velocity

BM: Lead velocity measures your monthly growth and qualified leads, thereby showing you the health of your pipeline development. The strength or weakness of the lead velocity rate helps you determine the impact on your bookings, recurring revenue, and cash. This is a good lead indicator for your business.

Churn

BM: Churn is an important SaaS metric. If you focus on mid-market and enterprise customers you can assess customer characteristics that indicate churn. This will help you proactively engage your customer success teams to reach out to customers and get the overall health status of their business with you. Assess your churn weekly and look at the traffic coming to your site. Try new methods to onboard your customers and make tweaks in your customer retention processes.

SaaS quick ratio

BM: This is good for customers who have an inbound go to market model where you've organic paid ads which drive traffic to your site. This metric measures your expansion vs contraction. A good SaaS quick ratio is greater than four. You'll be okay if you're 1-4. If it's less than 1 then you're contracting and in trouble. This might lead to trouble down the road. A good measure is to see each week where the net inflow or outflow of your ARR or MRR is going.

Customer acquisition cost

BM: During times like these, CAC ties up to the working capital of your business. Therefore, it's essential to find an efficient acquisition channel. This is the cost of ARR and will provide focus and discipline in your sales and marketing process by enabling them to focus on efficient channels. Also, it's good to remember that if your customers churn before they've paid the CAC, it just burdens your future customers causing a lot of working capital to get tied up.

AR aging

BM: AR aging is an area to focus on when cash gets tight. It determines how long each receivable has been on our books. This issue crops up when you invoice your customers, which causes cash collections to take up work. Implement weekly meetings to monitor AR aging with your team and determine which customers are at risk. This will show what actions need to be taken to so that you can collect on that account. If your customer is looking like a potential churn, then you can engage your customer success to see if you can do anything to salvage that account.

Improving payment collections during COVID

The next important area to look into is how to improve your collection processes. Many customers are impacted worse or in a better way during this situation. The ones who've been impacted badly need to be handled with absolute care. But, payment collections are important to keep your business health afloat. Henceforth, you need to bring in methods that will help you be sensitive to their situations and collect payments in a non-pressurizing way.

BM: If you're invoicing to a mid-market or an enterprise customer you need to send a PDF and emails, as they're not paying by credit cards. You need to be sensitive to their situation and not push hard. Balance a nice cadence of reaching out to your customers often. It's good to establish a process in your accounts receivables team on how often you're reaching out or receiving out to customers who're having difficulty paying. It's good to have weekly meetings to determine what is the next course of action for these customers.

Combating currency-fluctuations in cash-flow statements

With economies in crisis, many currencies are depreciating against the US dollar which is the benchmark in most cases. This isn't good news for many businesses, as it ties down to increased operational costs which seem to be escalating, thereby impacting cash-flows negatively.

BM: In cash management, you've currency issues. During these times, the currency fluctuations are more fluid. But, here's something you can do. If your business is working with a national bank, they'll be having a treasury division you can work with, in case you want to invest in any short-term securities. They can also give you advice on how to hedge against your native currency devaluation by having some policies put in place for that.

Driving clarity with data while treading murky waters

COVID-19's toll on businesses is undeniable. Businesses now have to quickly adapt and change according to the situation at hand. With a wide amount of data available it's easier to get lost in the data-pacific, and track metrics that don't add relevance to your business. Looking at how behaviors (market and consumer) are shifting will help you narrow down on metrics that matter. Though it's early to make definitive predictions on how the market is going to be or how the recovery is going to look like.

William Cordes, Founder, and CEO of KPI Sense, provides strategic finance solutions for early and late-stage SaaS businesses. Will drives clarity on where adjustments should be made in your short and long term strategies. He covers areas such as managing cash-burn, retention rates, and CAC.

Areas your business needs to look into

To propel your business forward, you need sustainable strategies driven by key metrics in place. The decision-making process in your business is going to coincide with your customers across industries. While some might seem to manage this crisis well, the others are going to be negatively impacted. This, in turn, will affect your revenue flow. To shield yourself from uncertainty, you need to gain a strong foothold in your business. Here's how you can do that

WC: The assumptions we're going to drive into calculating these metrics is that your business is working with businesses that are likely to be negatively impacted. But some businesses are accelerating and managing this crisis fairly well.

Customer success teams are adding additional value to their existing customers by providing flexibility for billings, payments, collections, and driving upsells. There is an evident freeze on new hiring and open requisitions.

Here's what companies can do to effectively manage their business during COVID-19

Metrics that matter now

Primarily companies tend to look at an array of metrics. But during times like these, you need to look at areas that matter, metrics that you can keep track of and take action in response.

Your areas of focus should be your operational, recurring revenue and sales metrics.

Operational Metrics

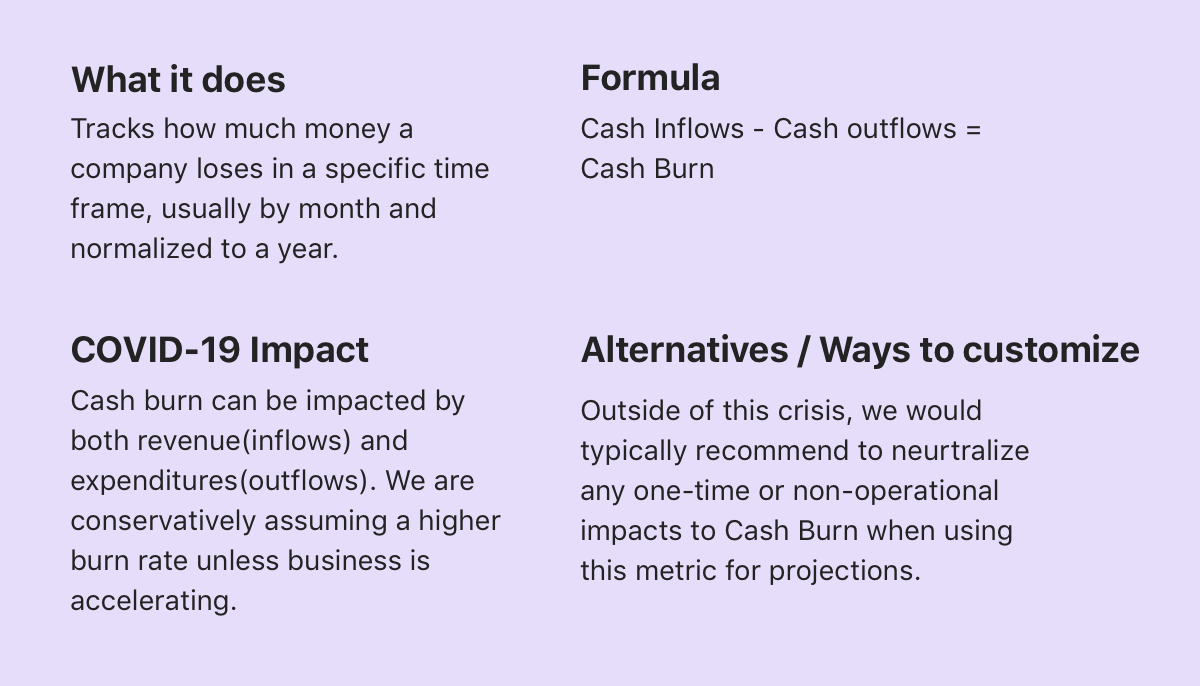

Cash burn

WC: One of the key points to be outlined here is about cash-burn and burn rate.

Even though there are going to be potential impacts on your revenue, the key lies in being flexible and reacting wisely from an expenditure standpoint. It's good to plan for the good and bad things and not assume we're going to have a V-shaped recovery. Practice conservatism and have 1-3 months of runaway. This is impactful if the current situation is going to linger longer.

If you're working with vendors in an affected space, reach out. You may be able to prepay or advanced pay around some of these expenses and probably negotiate a discount as well. Negotiating a 10-20% discount is going to be cash that's sitting on your balance sheet so that you can drive down your expense burden for the future.

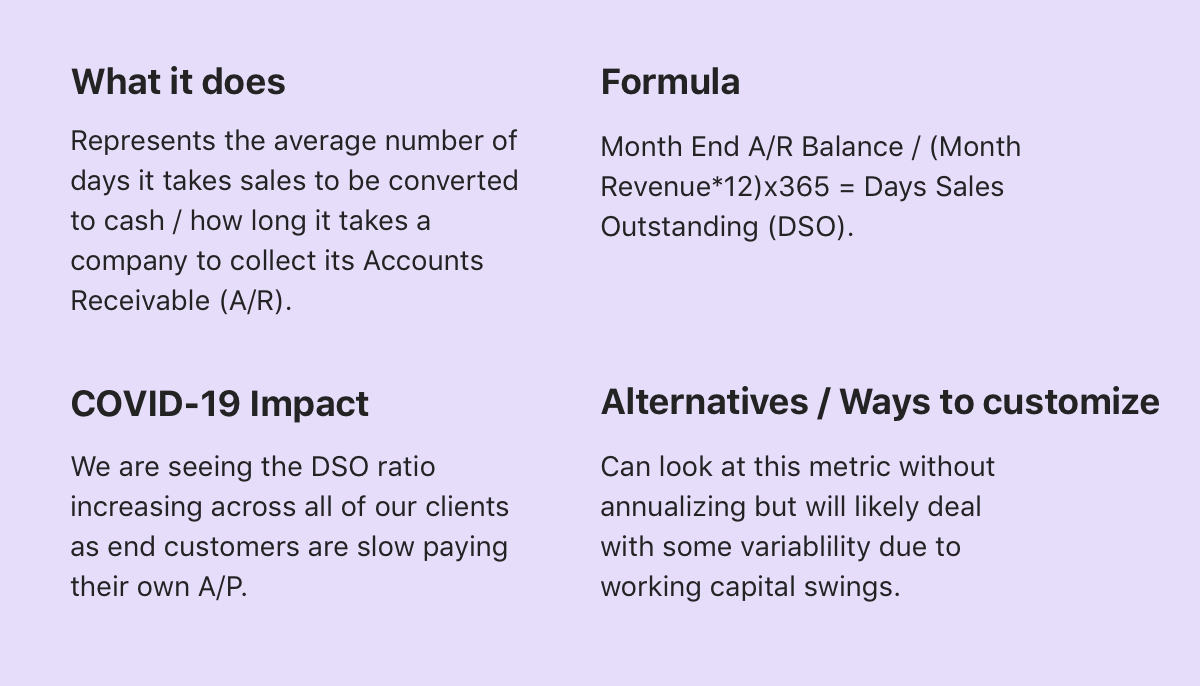

Sales outstanding

WC: Sales outstanding is basically calculating the time it takes for you to collect an invoice as it's sent out on average or what does that typically look like? The main reason why we focus on this metric is that it is one of the few things you can control. During these times, you can anticipate a slow down from a day sales outstanding standpoint.

This could be anywhere from 10-15 days. If you have a lot of enterprise customers, they might be paying on net 90 terms, and you'll know it's upwards of 90. If you get paid in 20 days, pre-crisis, depending on the business you're collecting from, it might be 30, 35 or 40 days moving forward. This is a huge impact-driver from the outlook of working capital. When you're forecasting ahead say 3-6 months from now, look at day sales outstanding.

Recurring revenue metrics

With a lot of uncertainty, many businesses are giving their customers to pause their subscriptions or provide delayed payment terms, extended trial versions, etc., These actions undertaken by your business can reflect on your revenue metrics.

WC: Companies are offering their customers paused engagement and providing temporary relief from a payment standpoint. These actions taken by companies actually lead to their dollars dropping. Even though we say it as contract expansion, it is technically a down-sell or a churned customer for the period they've ceased engagement with the product.

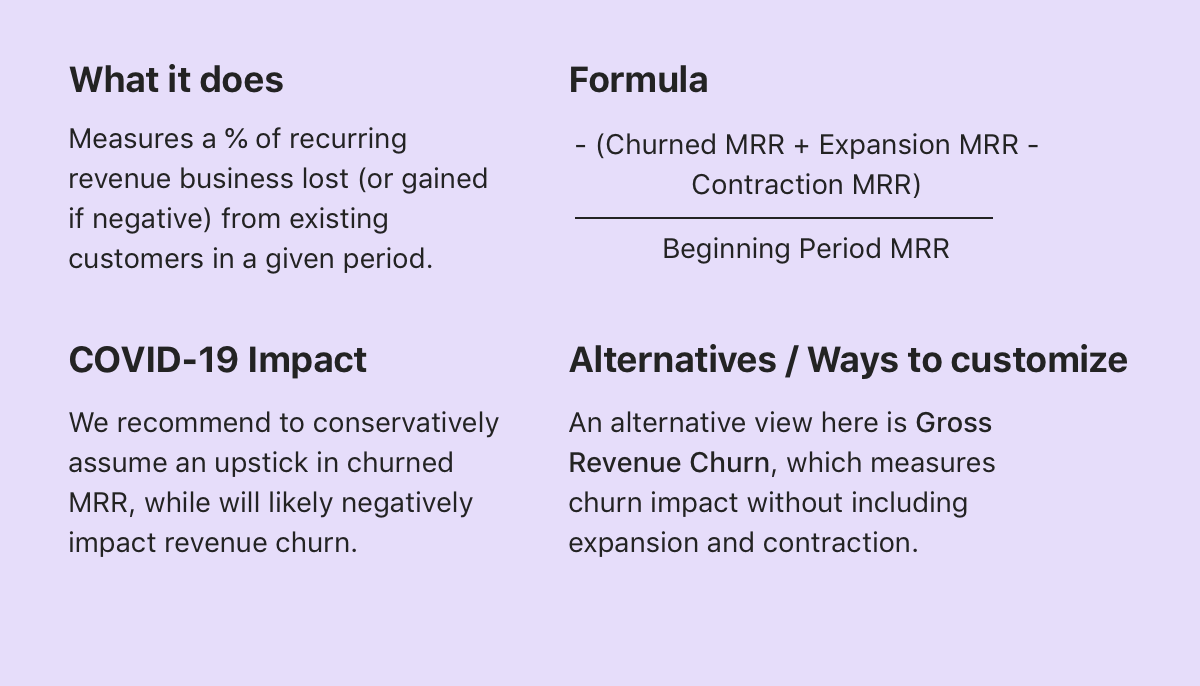

Churn metrics

WC: When talking about churn, I would like to classify it as net and gross revenue churn. Gross revenue churn is the churn you're going to have a hard time avoiding. But in net revenue churn, you have to factor in the expansion and contraction on how you can uplift and improve your revenue based with your existing customers.

You need to be proactive and focus on driving additional value. This will mitigate potentially some of the other churns that you may not be able to offset by bringing on new businesses or otherwise. In these times you need to look at how you can drive additional growth within your existing customer base.

Trend analysis and customer sub-segmentation

WC: This is one of the areas where we spend a lot of time. If you're able to clearly look at your data, this is one of the areas where we can potentially help. Drilling into this metric will help you

Identify where the churn is coming from

Narrow down of the particular part of the customer base

Identify sub-segments that are churning more than others

Analyzing these trends will help you to preemptively attack some of the causes. There are a lot of ways you can slice and dice this data. It can be based on

Your retention and churn data within these subsegments

Your customer size and geographical locations

The end-user industry you're serving

End-users your customers are serving

These points will help you generate insights that you can couple with your customer success strategy.

Sales and Marketing Metrics

Sales and marketing metrics are keys you need to keep a watch on. If something changes, you need to know where and how to focus and invest in areas that matter most now.

WC: If you see a big decrease in new bookings, you're likely going to face an increase in churn. If you're looking at trailing on a three-month basis, we might spread this potentially over to six months. For enterprise customers, we'll look at some of the data over the last 12 months. If you notice your customer acquisition cost spiking up, you need to focus on mitigating the cost and driving a more favorable investment from a marketing perspective.

When you're looking at lifetime value standpoint, it's good to ask

How long is the COVID crisis going to last? Is it something that's on for two months or is it something which might take 6 months?

How will this impact my business and impact my existing customers?

Then focus on evaluating this data, weekly, monthly and watch with a hawk's eye to see where things are changing.

While calculating customer acquisition costs, understand your payback period across different channels. If you see a marketing channel where the CAC is greater than the runway then try to minimize it. Focus on places you'll generate better ROI. Focus on areas where you can drive value and drive cash into areas where efficiency is guaranteed. The goal should be to either maintain your growth and protect you from potential loss from a revenue standpoint.

Should you or should you not upgrade your tech-stack now?

During these times it's better to focus on your collection mechanisms and payment flexibility. If any process is being automated it is directly proportional to the time saved. Small errors in calculations can lead to sloppy decisions. Considering the climate now, we need to be more vigilant with your numbers and eliminate manual errors.

WC: If there are ways to improve your collection and invoicing process by driving efficiency, you should go for it. Especially if it improves your AR collections process, which you need more of during these times. Also, considering the future, this is a huge area of focus and can drive a ton of value going forward.

Having data quality-related issues will give you incoherent metrics. Many companies have four different platforms using different tools. When there is no single point of truth it leads to improper metric calculations. There can be issues with their chart of accounts or data, but if your data doesn't flow across other sources there will be challenges that will be encountered.

To solve this, I think a good subscription management tool with visibility across channels can help drive normalcy and make things easier by aligning your metrics. This will be able to provide a central view of your financial data.

Managing Cash Flow the Chargebee way

With the economies tumbling, you need to make decisions for your subscription business, that'll keep you agile, sophisticated and resilient. You need to adapt and scale. For that, you need an effective subscription and billing system that'll scale along with you.

Karthik Srinivasan, Director of finance at Chargebee, shows how the platform can be used to track metrics that matter in real-time. He talks about the different scenarios which should be forecasted for and how to do it effectively using the tool. Listen to the webinar or read on to take away the key insights.

Recovery planning for post-COVID world

The post-COVID world is the most anticipated period for businesses. Many companies are looking at how their recovery will be. With many predictions being made which mostly lean towards a V-shaped recovery, but we're unable to tell for sure about the unknown. Uncalled for surprises in the world of finance spells chaos, which isn't good for your business. Therefore, planning for all the possible scenarios should be done.

KS: There are three different recovery scenarios we should be looking at. For those of you who're not familiar, the first recovery is V-shaped. This means you'll probably see a dip in your Q2 revenue, but by Q3, you'll be in a position to recover. The next is a W-shaped recovery. In this, you'll be seeing a dip in your Q2 revenue and will be anticipating a recovery in Q4.

The real worst-case scenario is the L-shaped scenario. In this, after the chaos, you see the growth to remain flat and recovery will be far-fetched during this year. These three scenarios should have a detailed revenue plan and spending pattern mapped so that you're prepared for whatever is set to happen.

Why should you model these scenarios?

KS: It is important to have a mechanism where we measure some of the business metrics. After your scenario planning is completed, you need to monitor key areas of your business weekly. Key metrics include MQL you generate, pipeline that is generated, new sales which are coming through, etc., You need a tracking mechanism that determines your cash flows in terms of the inflows and spend patterns of your business.

Why should you care about billing and a billing system during this scenario?

KS: Irrespective of the situation, it's important that you need to continue invoicing your customers. Invoicing is important from the receivables standpoint, now than ever, because it shows the money that flows into your business. By having a mechanism in place, you'll know for which invoices you can get paid for, depending on the payment terms agreed upon. Chargebee shows end-to-end metrics in real-time. Being the Director of Finance, it shows me regularly about "what's happening to our cash-flows", "how much money is coming through" and "how much time it takes for our customers to pay".

Looking at transactions from different dimensions

A single dimension of looking at your transactions don't tally during these uncertain times. You need to compare and contrast some metrics wrt to other metrics to really know how well you're. So, therefore, you need to look at details from different angles.

KS: You need to look at your cash inflows and your receivables in terms of how much your customers pay. You have to look at your metrics from different dimensions. Like, do you want to look at it from the transaction level or the customer level or the invoice limit? There are different dimension chains on how you can look out for information that addresses the need.

Let's walk through some of the real-time boards that Chargebee offers that'll help you understand this better: u through Chargebee's real-time boards that'll help you understand this better.

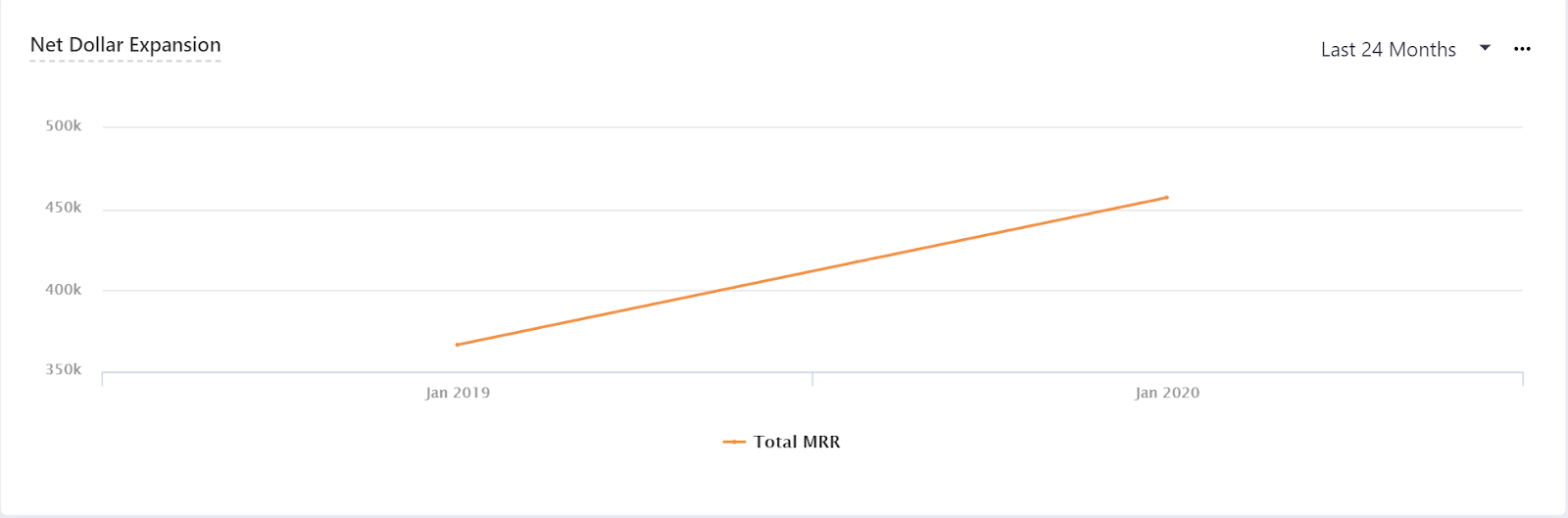

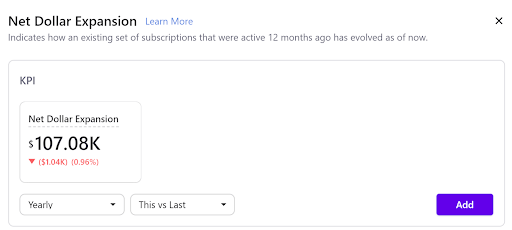

Chargebee's real-time cashflow board

The board above shows you how much cash you're burning through the month. In a cash flow metric, the first thing you need to know is how much cash you're burning. From a finance perspective, the above data, which tells us how much payments have come through the week. This helps us look at our cash balance and the inflow of net refunds. It gives you a quick insight in terms of how things are progressing. Thereby, helping us manage our cash flow better.

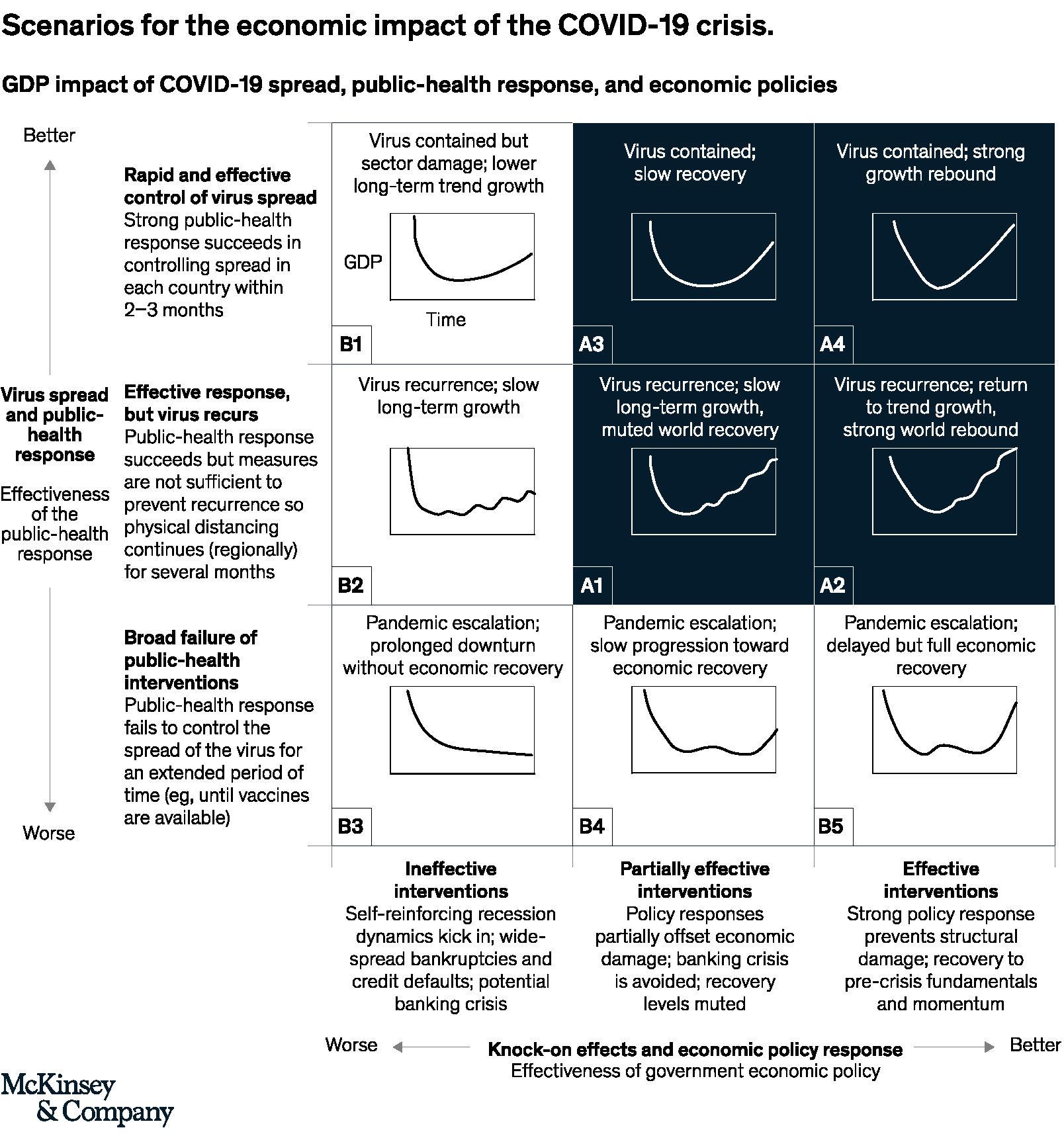

The next is your AR aging report. This report will show you signs of bad debt and how your company is progressing from the receivables PoV monthly.

Chargebee's real-time aging report

An AR aging report in real-time lets you see how much money your customers have paid, outstanding amounts and current debts. Aging reports help you understand if things in your business are going the right way, showing you if you've any financial baggage. It shows customers who're not paying you, probably it might be good to reach out to them and negotiate payment terms.

The next aspect to be considered is the Annual vs Monthly cash flows.

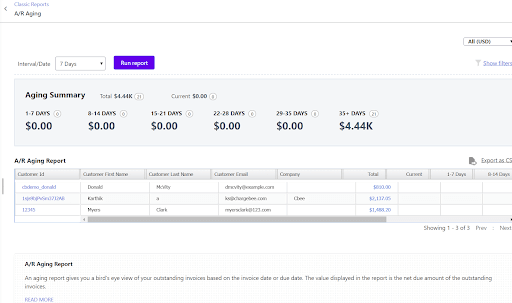

Gross cash-flow report

This report will help you predict which cash inflows are better. Reports like recurring vs non-recurring are important patterns to learn about your cash flows. You can see payments coming through different gateways and the kind of customers who're processing payments. It shows you which payments are semi-annual contracts that'll help you predict cash. Also, if you predict your cash flow then what do you anticipate for a month? Then, start measuring the actuals, weekly that'll show you, how well you're doing.

Metrics that matter

From a business standpoint, it's important to look at channels that are effective in bringing in ICP leads.

Acquisition channels

KS: Chargebee, shows you real-time reports on where leads are being generated. This will help you cut down costs in channels that don't matter at the moment. For example, previously paid ads would've been doing the trick, but now, socials will be the channel bringing you the leads. What this does is, show you where you can double down costs on channels that don't work right now, to channels that work. This will help you channel your cash to the right places. Not just this, you can analyze an array of metrics that'll show you how well you're doing right now.

Balancing growth and profitability

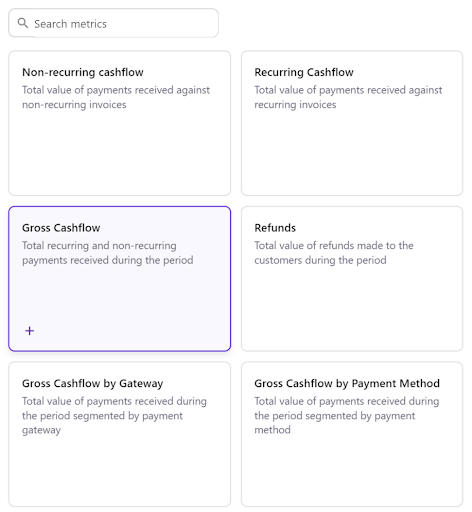

The next part you need to look at is your growth sustainability. Uncertain times like these call for a stable growth curve, which will keep your business afloat. But growth shouldn't be at the cost of profitability. If you acquire a customer with a higher CAC and low LTV, it means you're scaling but not profitably. Therefore, you need to look at metrics to keep your growth and profitability balanced to avoid overspending.

KS: One way to balance growth and profitability is by the rule of 40. If your growth rate plus EBITDA is 40% it means you're growing profitably. In this scenario, you should ensure that you're bringing in the right kind of customers and make sure that your retention is good.

The next area you need to analyze is if your growth is sustainable.

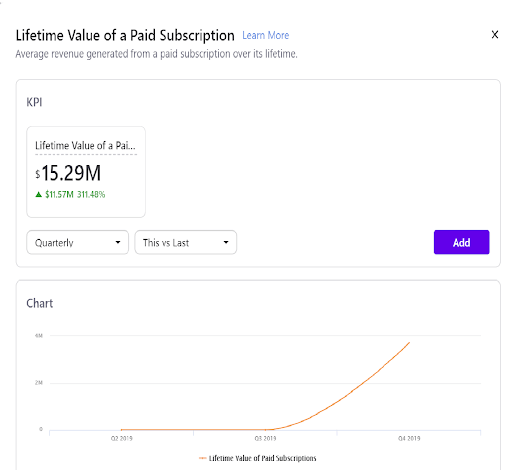

Sustainability vs profitability real-time reporting - Chargebee

KS: The advantage of an LTV metric is that it gives you an idea of your customers' quality. It also shows you how well you're able to retain them. If they look like they're churning you can nudge your success teams and learn the challenges they're going through. Maybe you can give them a discount, pause their subscriptions or perform actions that can increase their lifetime. Chargebee shows you how well you're able to retain your customers who came in a year ago and if you're able to scale and grow with them.

Questionnaire

What would be your recommendation to finance teams to maintain a single source of truth with metrics that matter?

KS: The first thing to do is to analyze the situation you're in. Then make a laundry list of metrics that is relevant to your business. Listing them as business metrics and cash flow metrics will help you set the stage to measure them. You need to know how your leads come through, how many leads you generate and the conversion pipeline for it. The first step is about setting the stage and then figuring out how to measure them.

How do you trade-off between discount vs payment terms?

KS: This is a contextual situation and depends on your relationship with the customer. The only challenge you'll be facing with discounts is that you don't want your customers to get used to that situation given the scope for it. In this case, offering payment terms is better. It is also slightly easier when compared to discounts. But this depends on the dollar value you're attributing to it. If you're giving a minuscule discount but retaining existing payment terms, then discounting works.

How does automation favor finance teams during times like these? KS: When working remotely, it's difficult for people to collaborate frequently. If you have an automated billing platform like Chargebee, it's easier to generate invoices for all the subscriptions you've seamlessly. Automation eases the friction in the ecosystem and makes it easier for employees working across different corners. Also, the best thing is, it is dynamic. We don't have to worry about missed payments, billings, collections, etc., which would be the case if tools like Chargebee ceased to exist.

Conclusion

Companies are now driving in a foggy situation at night. Shorter-term and flexible goals should be addressed now over longer-term forecasts. Your forecasting should be flexible and must help you to quickly pivot in the direction markets are going to take for recovery.

While closing new deals try to move into longer payment terms and contracts. This will give you more cash to operate in and pay for the expenses of your business. Ensuring a steady and visible cash-flow will help you stabilize your business during these uncertain times.

Right now, the main thing companies need to take into consideration is survival. Focussing on staying afloat and providing value by lowering your internal costs. High-value initiatives taken during this time can drive value to your business and build lasting relationships with your customers.

Doing business efficiently is important during these turbulent times. The right kind of subscription and billing tool eliminates friction in your finance ecosystem and makes decision making easier. It helps you narrow down on metrics and show real-time updates on how well you're performing so that you can react proactively. Your tool should bring in sophistication and agility and help you scale faster without being a cog in the wheel. Businesses should have systems in place that automates processes easing the miscommunications and mishaps that might happen in a remote working environment.